Notes And Analysis From Merck's Investor Day - 39 minutes read

Notes And Analysis From Merck's Investor Day - Merck & Co., Inc. (NYSE:MRK)

Notes And Analysis From Merck's Investor Day - Merck & Co., Inc. (NYSE:MRK)On June 20, Merck (MRK) held an investor day, its first in five years, to highlight its goals and objectives and provide a broad perspective on its five-year performance outlook. Although its blockbuster cancer treatment, KEYTRUDA (pembrolizumab), has been a spectacular success, investors have been concerned about whether the company has growth potential from other medicines in its pipeline, especially looking out to 2023 when the Januvia/Janumet franchise faces a steep slide in sales following patent expirations. During the presentation, management expressed confidence about the company’s growth prospects through 2023 and over the longer term.

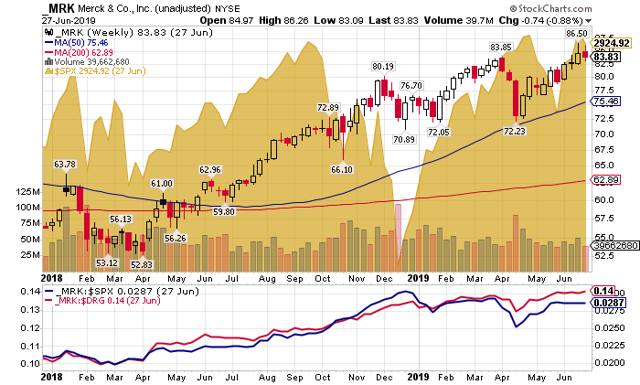

Investors have been pleased with the recent performance of Merck’s stock. Since the beginning of 2018 through June 27, it has delivered an annualized total return of 34.6%, much better than the S&P 500’s 8.4% total return. The gains over this period have more than made up for its underperformance vs. the S&P 500 from the March 2009 market bottom to the end of 2017. MRK has also outperformed its peers over the past 18 months, advancing 30.7% in price on an annualized basis, compared with the 6.4% gain by the NYSE ARCA Pharmaceutical Index ($DRG).

The major reason for Merck’s strong relative performance over the past 18 months was its outperformance during the December 2018 market sell-off, when the stock held its ground as the broader market plummeted. Merck’s stock has moved higher coming off the December lows, but it has not performed as strongly as the broader market. Technical indicators show that so far this year the stock has lost some of its upward momentum. A daily price chart raises the possibility of a near-term correction.

The loss of momentum may be a reflection of the stock’s higher valuation after the recent advance. The stock is currently valued at 18.6 times trailing 12-month non-GAAP earnings per share. That compares with its 2013-2018 average trailing P/E multiple of 15.1 times. Given the recent success of Keytruda, its miracle cancer drug, the market is willing to pay more for the anticipated higher earnings growth rate; but the stock may have risen to a point where the market is beginning to question whether future earnings growth can support its valuation.

Even so, management believes that Merck can deliver superior shareholder returns over the next few years. It sees three factors that can help it achieve strong shareholder returns going forward: sustained long-term revenue growth, meaningful operating margin expansion and balanced and disciplined capital allocation. It believes that it can deliver these returns despite the headwinds that it anticipates on pricing over the next few years from the increasing pressure to reduce drug costs for customers. Assuming management’s assertion that price declines will be manageable, my analysis suggests that the stock can deliver superior returns over the next few years.

Revenue Growth Expectations. This is the centerpiece of the company’s strategy. Merck is aiming to achieve growth across its four key focus areas: oncology, vaccines, hospital/specialty and animal medicines.

In 2018, Merck had total revenues of $42.3 billion, up 5.4% from 2017. This followed revenues gains of just 0.8% in 2016 and 2017 and a steady string of revenue declines from 2012 to 2015. Pharmaceutical revenues in 2018 increased 6.5% to $37.7 billion.

Oncology. Merck is driving global leadership with an oncology portfolio that is anchored by Keytruda and now includes Lynparza and Lenvima. Two other medications, Emend for post-chemotherapy nausea and Temodar for brain cancer are past patent expiry. Merck will also add PT2977, a novel late stage candidate for the treatment of renal cell carcinoma, when it completes its proposed $1.05 billion acquisition of privately held Peloton Therapeutics in the 2019 third quarter.

Keytruda is an anti-PD-1 (programmed death receptor-1) therapy that has been approved as a monotherapy for the treatment of certain patients with lung, skin, bladder, head and neck, stomach, kidney, lymph node and other cancers and in combination with chemotherapy in non-small-cell lung cancer (NSCLC).

Its demonstrated effectiveness has earned breakthrough drug designations (and accelerated approvals) from the FDA that have spurred rapid growth in sales. From a standing start in 2014, sales of Keytruda grew to $7.2 billion in 2018 and are on track to reach $10 billion in 2019.

Merck has so far won FDA approval for Keytruda’s use in 13 cancer types. The medicine has repeatedly demonstrated overall survival benefits in monotherapy and in combinations versus chemotherapy or other medicines in nearly all its clinical trials. The company believes that Keytruda may ultimately receive approvals for treatment in 25 or more cancer types. Thus, Keytruda sales are expected to grow at an elevated rate for at least the next few years.

Besides Keytruda, Merck has two other cancer medicines, Lynparza and Lenvima, which have demonstrated promising potential. Both drugs are being developed and marketed in collaborations – Lynparza with AstraZeneca and Lenvima with Eisai Co., Ltd. of Japan. Merck recognizes “alliance” revenue (i.e. its share of product sales less cost of sales and commercialization costs) with respect to both medicines.

Lynparza (olaparib) is an oral poly (ADP-ribose) polymerase (PARP) inhibitor indicated for certain ovarian and breast cancers in the U.S. and EU. Merck entered its collaboration with AstraZeneca in July 2017. Under the agreement, the companies share development and commercialization costs, but will independently explore opportunities in combinations with their respective PD-1 and PD-L1 medicines, Keytruda and Imfinzi. The two companies are also jointly developing another oncology medicine, selumetinib. They will share development and commercialization costs for Lynparza and selumetinib monotherapy and for non-PD-1/PD-L1 combination therapies. In 2018, Merck recognized $187 million of alliance revenue and $293 million of associated costs (e.g. milestone payment-related costs and SG&A expense) on Lynparza.

Lenvima (lenvatinib) is an orally available tyrosine kinase inhibitor currently approved in the U.S. for certain types of thyroid, liver and (in combination with Keytruda) kidney cancer. The drug has also been approved in the European Union, Japan and China to treat liver cancer (hepatocellular carcinoma). Under their March 2018 agreement, Merck and Eisai will jointly initiate clinical studies to evaluate Lenvima’s effectiveness (as monotherapy or in combination with Keytruda) in 11 potential indications of six types of cancer. Merck recorded $149 million of Lenvima alliance revenue and $1.54 billion of associated costs in 2018.

Vaccines. Merck has had very good success with its vaccines over the years. It sees numerous opportunities to address significant unmet needs by broadening and deepening its portfolio: serving new cohorts and geographies with its existing vaccines and developing new vaccines. Its current pipeline includes candidates aimed at ebola, pneumococcal virus (PCV), human respiratory syncytial virus (RSV), cytomegalovirus (CMV) and Dengue fever.

According to a complied forecast from several sources (Evaluate Pharma, IQVIA, DCVM and several other company reports), the vaccines market is forecasted to grow at a 5.5% compounded annual rate (with a range of 4.6%-6.4%) from an estimated $35 billion in 2018 to $55-$65 billion in 2028, driven by increasing penetration of inline products (in high income markets like the U.S. and EU), globalization and innovation. Merck’s five vaccines generated sales of $6.8 billion in 2018, up 10.4% from 2017.

Gardasil/Gardasil 9, which helps prevent certain diseases caused by some types of human papillomavirus (HPV), generated $3 billion in sales in 2018, up 36.5% from 2017, as its indications have expanded from younger (<27 years old) to older (27-45) men and women and into new geographies. Its Proquad/M-M-R II/Varivax vaccines for the prevention of measles, mumps, rubella and chicken pox posted sales of $1.8 billion in 2018, up 7.3%. Pneumovax 23 (pneumococcal disease) and RotaTeq (rotavirus) generated 2018 sales of $907 million (up 10.5%) and $743 million (up 6.1%), respectively.

A major disappointment has been Zostavax, a shingles vaccine, whose sales plummeted from $668 million in 2017 to $217 million in 2018, after the Advisory Committee on Immunization Practices (ACIP) of the Centers for Disease Control and Prevention (CDC) voted 8-7 to prefer GSK’s Shingrix.

Merck has two late stage vaccines in its pipeline: V920, for Ebola Zaire, is currently under review by the FDA. The investigational vaccine, which is licensed from NewLinks Genetics Corporation, received a Breakthrough Therapy designation from the FDA in 2016. Merck started the submission of a rolling Biologics License Application (BLA) for V920 in November 2018. Pre-licensure, investigational doses of V920 have been made available to support the response to recent outbreaks on an emergency basis. The vaccine has been reported to be 97.5% effective in people vaccinated between May 2018 and March 2019. While this clearly looks promising, the vaccine will likely be made available in most cases at low cost and the patent on V920 expires in 2023.

V114, an investigational polyvalent conjugate vaccine for the prevention of pneumococcal disease, is currently in Phase 3 trials. In January 2019, the FDA designated V114 as a potential Breakthrough Therapy in pediatric patients aged 6 weeks to 18 years for the prevention of invasive pneumococcal disease caused by two vaccine serotypes that are not addressed by Pfizer’s Prevnar 13 (PCV13), the current vaccine of choice for individuals up to 64 years old.

In May, Merck announced that a Phase 2 trial of V114 in infants met its primary endpoint by demonstrating an immune response for the two additional serotypes and non-inferiority to PCV13. The results support the continued progression of its broad clinical development program for V114 which currently includes 11 Phase 3 clinical trials.

If V114 continues to demonstrate an immune response for the two additional serotypes and at least non-inferiority to PCV13, it would therefore offer broader serotype coverage (15 vs. 13). According to Merck, those two additional serotypes (22F and 33F) plus the 13 covered by PCV13 would address roughly 40% of the incidence of residual pneumococcal disease (vs. less than 25% for PCV13 alone), across pediatric and adult populations.

However, competition is not standing still, so it remains to be seen whether V114 will demonstrate sufficient superiority to take meaningful share from PCV13 and whether it can become established before competing formulations find their way to market.

The success of V114 could also affect sales of Pneumovax 23. Despite the superior commercial success of Prevnar 13, Pneumovax 23 offers a unique value proposition: broader serotype coverage (in 23 serotypes) at a lower cost. Pneumovax 23 is recommended by the CDC for those aged 19-64 who have certain chronic conditions, such as diabetes, heart disease or COPD. It is also recommended by the CDC for those who are 65 and older, even if they have previously received a dose of another pneumococcal vaccine. V114 is presumably more effective than Pneumovax 23 for the 15 serotypes that both vaccines cover. Consequently, it is likely that the success of V114 will come at some expense to Pneumovax 23.

Besides V114, Merck has, in an earlier stage of development, V116, which aims to broaden protection in the adult population to even more serotypes. It also has other early stage PCV candidates targeting the broadest possible protection for the pediatric population.

Beyond PCV, Merck has multiple vaccine programs targeting three diseases: (1) human respiratory syncytial virus (RSV), a viral infection affecting the respiratory system; (2) cytomegalovirus (CMV), which is passed congenitally in up to 2.0% of the population and also affects HIV-positive individuals with symptoms ranging from fever, fatigue, muscle/joint pain and hearing loss, among others; and (3) Dengue fever, which may infect as many as 400 million people worldwide each year. The company estimates the global market potential of viruses targeting these diseases to be about $10 billion, including $5 billion for RSV, more than $3 billion for CMV and more than $3 billion for Dengue. It says that its V160 candidate for CMV has the potential to be first in class and its V181 data shows the potential to cover four Dengue serotypes with one dose.

Hospital/Specialty. I am assuming that this broad category covers Merck’s Hospital Acute Care, Hepatitis, HIV and Immunology franchises. (It does not, I believe, include Merck’s Cardiovascular, Diabetes, Women’s Health and General Medicine franchises.) By that definition, Hospital/Specialty had identifiable sales (from nine specific medicines) of $6.2 billion, down 18% from 2017. The segment suffered a 72% plunge in sales of Zepatier, a hepatitis C drug, which has lost out to tough competition. It also saw declines in 2018 sales in five other medicines (Isentress (HIV), Cubicin (antibiotic), Cancidas (antifungal), Invanz (for certain infections) and Remicade (anti-inflammatory)) due either to competition or patent expiry.

On the positive side, Merck saw growth in 2018 sales of Bridion (used post-surgery for the reversal of two neuromuscular blocking agents), Noxafil (for fungal infections) and Simponi (anti-inflammatory).

Despite the drop in sales, Hospital/Specialty remains a priority for Merck. I will focus here on Hospital/Specialty’s late stage pipeline.

HIV is still a major global health threat with an estimated 37 million people living with the virus and nearly one million HIV-related deaths in 2017. Merck is continuing its 30 years of innovation in antiretroviral therapies, building upon its success with Isentress, which had sales of $1.14 billion in 2018, down 5.3% from 2017. Its most advanced compound, MK-8591, is currently in a Phase2B trial (in combination with Doravirine and Lamivudine). MK-8591 has a unique pharmacology that may enable longer duration dosing (monthly oral or implantable) for prevention and daily or weekly doses for treatment. This could help address the problems of missed daily doses and pill fatigue that often thwarts the effective treatment of the disease. Besides MK-8591, Merck has many other mechanisms for HIV treatment in development.

MK-7264 (gefapixant) is a selective, non-narcotic, orally-administered P2X3-receptor antagonist that is under investigation in a Phase 3 trial for the treatment of refractory, chronic cough and in a Phase 2 trial for the treatment of women with endometriosis-related pain (especially associated with menstruation). Merck gained the rights to gefapixant with its acquisition of Afferent Pharmaceuticals in 2016. Through current and other planned clinical trials, Merck is exploring the role of the P2X3 pathway in sensory pathology disorders. Besides chronic cough and endometrial-related pain, it is investigating the technology as a treatment for sleep apnea.

Accordingly, the potential market for gefapixant is big: Chronic cough is prevalent in 10% of the global population, of which about 20% have either refractory (i.e. unyielding to treatment) or unexplained chronic cough. Endometrial-related pain affects an estimated 176 million women worldwide. About 29 million Americans suffer from sleep apnea.

Other potential applications for gefapixant and/or its derivatives include headaches/migraine, hypertension, irritable bowel syndrome (with constipation), neuropathic pain and muscle pain. Blocking the P2X3 receptors may eliminate the afferent nerve fibers or vessels that send out aberrant signals of disease with the goal of restoring normal sensory function.

If successful, MK-7264 could reduce the use of opioids in the treatment of pain. According to Merck, MK-7264 may also be helpful in reducing the accumulation of toxic proteins that is associated with diseases such as Alzheimer’s disease and amyotrophic lateral sclerosis (ALS), which is also known as Lou Gehrig’s disease.

MK-1242 (vericiguat) is a potential treatment for heart failure that is currently under investigation in a Phase 3 trial with patients suffering from chronic heart failure (CHF) with reduced ejection fracture (when the heart does not pump out blood normally (aka systolic heart failure)). It is also being tested in a Phase 2 clinical trial in patients with preserved ejection fracture (when the heart does not fill properly with blood (aka diastolic heart failure)). Vericiguat is being developed in a collaboration with Bayer AG.

MK-7655A (relebactam+imipenem/cilastatin) is a combination of relebactam, an investigational beta-lactamase inhibitor, and imipenem/cilastatin, an approved “super” antibiotic currently sold under the brand name Primaxin. It is under investigation as a treatment for complicated urinary tract and intra-abdominal infections in adults caused by certain susceptible Gram-negative bacteria that are highly resistant to treatment and for which there are no or limited alternative therapies available. The FDA accepted Merck’s new drug application (NDA) for MK-7655A for Priority Review in February 2019. The PDUFA date (the date by which the FDA must respond to Merck’s NDA under the Prescription Drug User Fee Act) is July 16, 2019.

Merck has previously announced that a Phase 3 study of MK-7655A had met its primary endpoint by demonstrating a favorable overall response in the treatment of imipenem-non-susceptible bacterial infections. In addition, MK-7655A met its secondary endpoint by demonstrating lower treatment-emergent kidney toxicity.

Besides the two infection indications listed above, the FDA had previously designated MK-7655A as a Qualified Infectious Disease Product and gave it Fast Track status for the treatment of hospital-acquired bacterial pneumonia and ventilator-associated bacterial pneumonia.

In April, Merck completed the acquisition of Immune Design for $300 million. Immune Design is a late-stage immunotherapy company that employs in vivo approaches that enable the body’s immune system to fight disease. Its proprietary GLAAS and ZVex technologies help activate the immune system’s natural ability to generate antigen-specific cytotoxic immune cells to fight cancer and other chronic diseases.

Animal Health. Merck Animal Health (MAH) is a market leader in global animal health, with revenues of $4.2 billion in 2018, up 8.7% from 2017. 38% of 2018 revenues were from companion animal (e.g. dogs and cats) products and services; the remaining 62% were from livestock. Only 29% of its revenues came from the U.S. According to Merck’s own figures (and my calculations), MAH’s revenues (presumably net of divestitures) grew at an average annual rate of 9.2% from 2014 to 2018, better than global industry growth of 5.5%.

MAH estimates current worldwide animal health industry sales of more than $34 billion are growing at a mid-single-digits rate. It believes that major global trends, like population growth, rising incomes and increasing urbanization, will continue to support growth in demand for animal health products. Going forward, MAH believes that its revenue growth will continue to outpace the industry.

MAH focuses on the development and deployment of innovative products and technologies that help improve the productivity (and profitability) of its customers’ operations. Key product areas include pharmaceuticals, vaccines, health management solutions and emerging digital technology. It has a robust new product development network, with dedicated research centers for pharmaceuticals and biologicals in many countries, a strong collaboration with Merck Research Laboratories and many external partnerships. That network delivered 66 product approvals from 2014-2018 and more than 150 licenses to expand sales into new geographies.

MAH is a leader in animal health vaccines. Strong growth in global sales were driven in 2018 by its Bravecto line of flea and tick products for cat and dogs and higher sales of companion animal vaccines. Growth in livestock revenues came from ruminant (e.g. cows and sheep), poultry and swine products.

MAH is pursuing high growth opportunities. Besides vaccines and pharmaceuticals, it is developing innovative (pharmaceutical) delivery technologies that improve the effectiveness of administering medicines to ensure that animals receive the full and proper doses in a timely manner.

In April, Merck completed the acquisition of privately held Antelliq Group for €3.25 billion, including €1.15 billion of assumed debt. Antelliq is a leader in digital animal identification, traceability and monitoring solutions that help veterinarians, farmers and pet owners gather critical data to improve the management, health and well-being of livestock and pets. Growing global demand for protein (i.e. meat) is driving the increasing use of digital technology to support food safety (through food traceability and disease detection) and productivity in animal agriculture. Antelliq’s systems facilitate the monitoring of critical health issues, such as animal fertility and disease, across entire herds. Its identification, tracking and intelligence solutions promote sustainable resource management of fish populations and aquaculture. Its pet door and feeders help pet owners manage food intake and access to indoor/outdoor spaces. Antelliq had revenues of €300 million in the twelve months ended Sept. 30, 2018. MAH believes the business has significant growth potential.

Revenue Summary and Projections. Merck’s 2019 guidance anticipates revenues of $43.9 to $45.1 billion, up 5.2% at the midpoint of the range. Going forward, my projections suggest that Merck’s revenue growth will pick up to about 6.5% in 2020 and 2021, ease to about 5.0% in 2022 and then fall back to flat (i.e. zero) in 2023. My projections assume that sales of Keytruda will grow steadily to about $14 billion in 2023 and that alliance revenue for Lynparza and Lenvima will grow to $2.0 to $2.5 billion each (or $4.0 to $5.0 billion total) in 2023. I assume modest contributions (less than $1 billion each) from the pipeline (including V114, MK-7624, MK-1242 and MK-7655A) and that the growth in sales of V114 will be offset in part by declining sales of Pneumovax 23.) My projections anticipate 2023 revenues of $1.5 billion for PT2977, acquired with Peloton Therapeutics, (primarily because of Merck’s $1.05 billion up front acquisition cost). I also assume that Animal Health revenues will grow at a compounded annual rate of 8% through the forecast period.

My revenue projections are not in line with management’s long-term guidance, given at the analyst meeting, which anticipates “strong” revenue growth every year, even including 2023 which will be the year of the greatest impact from Januvia’s loss of exclusivity. (Given Merck’s recent history and industry trends, I believe that annual revenue growth above 5% should be considered quite strong, especially in light of likely industrywide pricing pressure (more about that later)).

My projections do not reflect management’s guidance for 2023. In that year, I anticipate that sales from the Januvia franchise (Januvia and Janumet) will fall by roughly 50% or $3 billion. So in order for 2023 revenues to grow at the strong rate of say 5%, Merck would have to generate incremental revenues of about $5.6 billion, making up for the $3 billion loss of revenues and adding an additional $2.6 billion in revenues to achieve a 5% growth rate.

I am not suggesting that the company will not be able grow revenues by $5.6 billion in 2023. Rather, I am saying that I do not have enough information to project >5% sales growth in 2023 with a reasonable degree of confidence. Five years is, after all, a long way off, and I do not have the specific knowledge of the sales growth potential of individual drug candidates to project stronger sales growth for the current crop of late-stage compounds for 2023. Additional new compounds that were not discussed at the analyst meeting may very well contribute meaningfully to 2023 results. Merck will probably also make additional acquisitions which can offset some of the future decline in Januvia sales.

My projections assume (and management’s guidance implies) modest and manageable price declines over the forecast period. At the analyst meeting, management said that it expects that average prices will decline over the next five years, but that should not prevent it from achieving its revenue targets. Merck’s U.S. Pricing Transparency Report indicates that both list and net price increases have been moderating in recent years. According to that report, Merck’s average net price for pharmaceuticals increased 3% in 2018 after falling 1.9% in 2017 and its average discount from list price increased from 27% in 2010 to 44% in 2018. My projections implicitly assume that there will be no sudden negative change in industrywide pricing and that modest declines in prices throughout the forecast period will be more than offset by net volume increases on existing medicines and sales from new drug launches.

Investors should also recognize that the sales performance of individual drugs can sometimes be subject to significant and surprising changes, both on the upside and downside. While I, along with most analysts, recognized that Keytruda had the potential to be a blockbuster medicine, I did not anticipate it would become a juggernaut. Similarly, I did not predict the disappointing performance of both Zostavax and Zepatier. There will undoubtedly be future surprises in Merck’s product portfolio and pipeline; but those who invest long-term in Merck have to believe that the company’s leading position in proprietary medicines combined with the broad diversification of its product portfolio (even with the outsized growth of Keytruda) will insulate it from a sharp decline in revenues and profits. By virtue of its constant surveillance of the global pharmaceuticals market, Merck has over the years demonstrated an ability to spot emerging challenges and opportunities in its product portfolio and make adjustments as required.

Other Components of the Financial Projections. While revenues are a key driver of Merck’s profitability, costs are also of course a major contributor. As the company remains focused on driving revenue growth, it is also paying close attention to its operating costs.

Merck aims to become a leaner and more efficient company. It will continue to focus its people and resources on the greatest opportunities for growth, tweaking its operating model and corporate culture to become more agile and efficient. Besides gaining the flexibility to respond more quickly to opportunities and challenges as they arise, the company wants to retain the capacity for first-mover advantage to anticipate and capitalize on the next wave of industry innovation (or change).

As part of this effort, Merck has been embracing new digital capabilities (including automation) to better enable innovation, expand customer and patient reach and reduce supply chain and back office costs. It expects to reduce (non-GAAP) operating costs as a percent of sales over the next few years, raising its (non-GAAP) operating margin and increasing its return on invested capital.

During the first quarter, Merck approved a new global restructuring program to further optimize its manufacturing and supply network and reduce its global real estate footprint. This program builds on its previous restructuring initiatives. This program is expected to cost $800 million to $1.2 billion (pre-tax) and be completed by 2023. Merck’s guidance for 2019 anticipates $500 million of restructuring costs.

The overall anticipated improvement in profits and profitability should help generate significant free cash flow over the next five years, which Merck plans to allocate to investments (R&D, bolt-on acquisitions, strategic collaborations, targeted manufacturing capacity increases and IT infrastructure upgrades) and shareholder returns ( dividends and stock buybacks). It is targeting a dividend payout ratio of 47%-50% over time.

If all goes as planned, the achievement of sustained long-term revenue growth, operating margin expansion and value-creating capital allocation should help drive both future growth in revenues and profits and attractive shareholder returns.

Earnings Projections, Valuation and Impact of GAAP vs. Non-GAAP. Like most companies, Merck reports non-GAAP numbers to help investors better understand its performance. I typically use GAAP numbers as the primary measure of a company’s historical performance and non-GAAP adjustments as an aid in forecasting future profits (under the assumption that the adjustments are unusual and will go away over time).

Merck’s non-GAAP adjustments typically fall into two categories: acquisition-related costs (including costs associated with collaborations) and restructuring costs. I believe that adjusting historical costs for some acquisition-related costs – for example, the non-cash charges associated with acquired in-process research and development costs – are appropriate. Restructuring costs, on the other hand, should continue to be included in evaluating Merck’s profitability, because they have been ongoing for more than a decade and will likely continue in the future.

In 2019, Merck’s non-GAAP adjustments totaled $5.4 billion or $2.02 per share. Of that amount, roughly $2.87 billion was attributable to acquisitions, $1.97 billion was attributable to collaborations and $0.61 billion was attributable to restructuring costs. By comparison, 2018 non-GAAP adjustments totaled $8.5 billion or $3.12 per share. These non-GAAP costs appear in each of Merck’s expense line items, including cost of sales, SG&A expense, R&D expense and restructuring costs.

In its 2019 guidance, management expects that non-GAAP adjustments (for acquisition and the $500 million of restructuring costs) will total $1.675 billion or $0.65 per share. That is down significantly from the prior years, but not surprising given the slowdown in acquisition activity. (Yet, it remains to be seen whether Merck’s GAAP guidance will change following the recent acquisitions of Antelliq, Peloton Therapeutics and Tilos Therapeutics (announced in June).

At the analyst meeting, management said that it expects that the company’s non-GAAP SG&A expense and non-GAAP R&D expense will decline steadily over time, so that its non-GAAP operating margin will increase and lead to improved returns on invested capital. Management’s guidance applies to non-GAAP operating costs because it is impossible (or at least extremely difficult) to forecast acquisition and collaboration costs for transactions that have not yet taken place.

My 2019-2023 projections, which are based off of management’s 2019 guidance, assume steady improvement in Merck’s GAAP pre-tax profit margin from 28.3% in 2019 to 30.6% in 2023. I also assume that non-GAAP expenses will remain fixed at $1.675 billion per year (after-tax) over the forecast period. Since restructuring costs are expected to decline, this implies that non-GAAP acquisition costs will go up, but only modestly during the forecast period and remain well below what they were over the past three years (from 2016 to 2018).

Those assumptions for non-GAAP acquisition costs will probably turn out to be wrong, but it should not negate my forecast of improved performance as long as future acquisitions and collaborations are profitable (i.e. they deliver more revenues than costs, including the non-GAAP acquisition costs, over time). Given the nature of the R&D cycle, it is almost certainly the case that acquisitions hurt profitability in the short run during the early stages of new drug development, but they should boost profitability in the long run.

With that caveat, my projections anticipate that Merck’s GAAP earnings per share will grow from $4.07 in 2019 to $5.87 in 2023. I project that its non-GAAP earnings will grow from $4.72 in 2019 to $6.60 in 2023. At 50% of GAAP EPS, I anticipate that its dividends per share will grow from $2.20 currently to $2.94 in 2023.

According to my model, the assumed P/E multiple in 2023 is the key to determining shareholder returns over the forecast period. Like most pharmaceutical stocks (I believe), Merck’s stock value is typically calculated using non-GAAP EPS. As noted above, the stock is currently trading at 18.6 times trailing 12-month non-GAAP EPS (or 20.6 times GAAP EPS). If I assume that the non-GAAP P/E multiple compresses to 16 (or 18 on a GAAP basis), Merck’s stock would rise to $105.60 in 2023. Together with anticipated dividends, the stock would deliver a total annualized return of just over 9%. If there is no compress-ion in the P/E multiple in 2023, my model shows a total annualized return of just over 13%.

It is reasonable to expect some reduction in the multiple by the end of the forecast period because it is likely that Keytruda’s revenues will be flattening out and its patent expires in the U.S. and EU in 2028.

While I believe that my projections are reasonable, it is important to recognize that my projections for both Merck’s revenue growth and its operating margins are well above their recent historical averages. As already noted, however, my projections are consistent with and show only modest improvement over management’s guidance for 2019.

My projections are also heavily dependent upon Keytruda and Merck’s oncology franchise. My forecasts assumes $8 billion of incremental revenues for Keytruda, Lynparza and Lenvima by 2023, accounting for more than 100% of the company’s total revenue growth over the forecast period. Essentially, I am assuming that growth in the existing portfolio will be offset by declines mostly from patent expirations, including the loss of exclusivity for the Januvia/Janumet franchise in 2023.

Despite the risks, therefore, I believe that on balance there is strength in Merck’s current portfolio and management has sufficient optionality to deliver improved financial performance for the company and solid returns to shareholders over the forecast period.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Source: Seekingalpha.com

Powered by NewsAPI.org

Keywords:

Merck & Co. • Merck & Co. • New York Stock Exchange • M. R. Krishnamurthy • M. R. Krishnamurthy • Pembrolizumab • Pembrolizumab • Pipeline transport • Sitagliptin • Sitagliptin/metformin • Patent • Consumer confidence • Company • Economic growth • Investment • Stock • S&P 500 Index • Total return • S&P 500 Index • M. R. Krishnamurthy • NYSE Arca • Reason • Market (economics) • Market (economics) • Market (economics) • Stock • Price • Momentum (finance) • Stock • Valuation (finance) • Stock • Accounting standard • Earnings per share • Pembrolizumab • Market (economics) • Economic growth • Stock • Market (economics) • Futures contract • Valuation (finance) • Management • Merck & Co. • Shareholder • Rate of return • Factors of production • Shareholder • Return on investment • Sustainability • Term (time) • Revenue • Economic growth • Operating margin • Economic growth • Capital (economics) • Economic system • Return on investment • Pricing • Cost • Customer • Management • Price • Stock • Return on investment • Revenue • Economic growth • Merck & Co. • Oncology • Vaccine • Pharmaceutical drug • Merck & Co. • Revenue • Pharmaceutical drug • Revenue • Oncology • Merck & Co. • Oncology • Pembrolizumab • Pharmaceutical drug • Chemotherapy • Nausea • Temozolomide • Brain tumor • Patent • Merck & Co. • Renal cell carcinoma • Platoon • Therapy • Pembrolizumab • Programmed cell death protein 1 • TNF receptor superfamily • Therapy • Combination therapy • Therapy • Patient • Lung • Skin • Urinary bladder • Head and neck cancer • Stomach • Kidney • Lymph node • Cancer • Combination therapy • Chemotherapy • Non-small-cell lung carcinoma • Non-small-cell lung carcinoma • Efficacy • Breakthrough therapy • Food and Drug Administration • Pembrolizumab • S postcode area • Merck & Co. • Food and Drug Administration • Pembrolizumab • Cancer • Anticoagulant • Medicine • Survival rate • Combination therapy • Chemotherapy • Clinical trial • Pembrolizumab • Therapy • Cancer • Anticoagulant • Pembrolizumab • Mortality rate • Pembrolizumab • Merck & Co. • Cancer • Pharmaceutical drug • Pharmaceutical drug • AstraZeneca • Eisai (company) • Japan • Merck & Co. • Revenue • Cost of goods sold • Olaparib • Adenosine diphosphate ribose • DNA polymerase • Poly ADP ribose polymerase • Enzyme inhibitor • Ovarian cancer • Breast cancer • Cancer • European Union • Merck & Co. • AstraZeneca • Economic development • Renewable energy commercialization • Programmed cell death protein 1 • PD-L1 • Pembrolizumab • Oncology • Medicine • Selumetinib • Drug development • Selumetinib • Combination therapy • Programmed cell death protein 1 • PD-L1 • Merck & Co. • Revenue • SG&A • Lenvatinib • Tyrosine-kinase inhibitor • Anticoagulant • Thyroid • Liver • Combination therapy • Pembrolizumab • Renal cell carcinoma • Pharmaceutical drug • European Union • Japan • China • Hepatocellular carcinoma • Hepatocellular carcinoma • Merck & Co. • Eisai (company) • Clinical trial • Efficacy • Combination therapy • Combination therapy • Pembrolizumab • Indication (medicine) • Anticoagulant • Cancer • Merck & Co. • Vaccine • Merck & Co. • Vaccination • Vaccine • Vaccine • Ebola virus disease • Streptococcus pneumoniae • Hematocrit • Human respiratory syncytial virus • Human respiratory syncytial virus • Cytomegalovirus • Cytomegalovirus • Dengue fever • Pharmaceutical industry • Vaccine • European Union • Globalization • Innovation • Merck & Co. • Vaccine • S68 (Rhine-Ruhr S-Bahn) • Gardasil • Gardasil • Disease • Symptom • Human papillomavirus infection • Human papillomavirus infection • Varicella vaccine • Vaccine • Preventive healthcare • Measles • Mumps • Rubella • Chickenpox • Streptococcus pneumoniae • Rotavirus vaccine • Rotavirus • Zoster vaccine • Zoster vaccine • Advisory Committee on Immunization Practices • Advisory Committee on Immunization Practices • Centers for Disease Control and Prevention • Centers for Disease Control and Prevention • GlaxoSmithKline • Merck & Co. • Vaccine • Pipeline transport • Ebola virus disease • Zaire • Systematic review • Food and Drug Administration • Investigational New Drug • Vaccine • Genetics • Breakthrough therapy • Food and Drug Administration • Merck & Co. • Biologics license application • Biologics license application • Investigational New Drug • Epidemic • Emergency medicine • Vaccine • Vaccination • Patent • Conjugate vaccine • Preventive healthcare • Streptococcus pneumoniae • Phases of clinical research • Clinical trial • Food and Drug Administration • Action potential • Breakthrough therapy • Pediatrics • Patient • Ageing • Preventive healthcare • Streptococcus pneumoniae • Vaccine • Serotype • Pfizer • Pneumococcal conjugate vaccine • Vaccine • Merck & Co. • Phases of clinical research • Clinical trial • Infant • Clinical endpoint • Immune response • Serotype • Drug development • Phases of clinical research • Clinical trial • Immune response • Serotype • Merck & Co. • Incidence (epidemiology) • Streptococcus pneumoniae • Pneumococcal conjugate vaccine • Unique selling proposition • Serotype • Centers for Disease Control and Prevention • Ageing • Chronic condition • Diabetes mellitus • Cardiovascular disease • Chronic obstructive pulmonary disease • Centers for Disease Control and Prevention • Pneumococcal vaccine • Serotype • Vaccine • Merck & Co. • SMS V116 • Serotype • Pneumococcal conjugate vaccine • Pediatrics • Pneumococcal conjugate vaccine • Merck & Co. • Vaccine • Disease • Human respiratory syncytial virus • Human respiratory syncytial virus • Viral disease • Respiratory system • Cytomegalovirus • Cytomegalovirus • Symptom • Fatigue (medical) • Myalgia • Arthralgia • Hearing loss • Dengue fever • Virus • Disease • Human respiratory syncytial virus • Cytomegalovirus • Dengue fever • Cytomegalovirus • Dengue fever • Serotype • Acute care • Hepatitis • HIV • Immunology • Merck & Co. • Circulatory system • Diabetes mellitus • Women's health • Internal medicine • Elbasvir/grazoprevir • Hepatitis C • Pharmaceutical drug • Pharmaceutical drug • Raltegravir • HIV • Daptomycin • Antibiotics • Caspofungin • Antifungal • Ertapenem • Infection • Infliximab • Anti-inflammatory • Patent • Merck & Co. • Neoplasm • Sugammadex • Surgery • Neuromuscular-blocking drug • Mycosis • Golimumab • Anti-inflammatory • Specialty (medicine) • Merck & Co. • HIV • Global health • Virus • HIV • Deaths in 2017 • Merck & Co. • Management of HIV/AIDS • Therapy • Raltegravir • Clinical trial • Combination therapy • Doravirine • Lamivudine • Pharmacology • Oral administration • Preventive healthcare • Dose (biochemistry) • Therapy • Dose (biochemistry) • Pill (pharmacy) • Fatigue (medical) • Disease • Merck & Co. • Mechanism of action • HIV • Drug development • Binding selectivity • Narcotic • Oral administration • P2RX3 • Receptor antagonist • Phases of clinical research • Clinical trial • Disease • Cough • Phases of clinical research • Clinical trial • Endometriosis • Pain • Menstruation • Merck & Co. • Learning • Lymphatic vessel • Pharmaceutical drug • Clinical trial • Merck & Co. • P2RX3 • Cell signaling • Sensory nervous system • Pathology • Disease • Cough • Endometrium • Pain • Therapy • Sleep apnea • Action potential • Cough • Disease • Therapy • Cough • Endometrium • Pain • Sleep apnea • Action potential • Polymerase chain reaction • Derivative (chemistry) • Headache • Migraine • Hypertension • Irritable bowel syndrome • Constipation • Neuropathic pain • Myalgia • Receptor antagonist • P2RX3 • Receptor (biochemistry) • Afferent nerve fiber • Nerve • Blood vessel • Cell signaling • Disease • Sensory nervous system • Opioid • Therapy • Pain • Merck & Co. • Toxicity • Protein • Disease • Alzheimer's disease • Amyotrophic lateral sclerosis • Amyotrophic lateral sclerosis • Amyotrophic lateral sclerosis • Action potential • Therapy • Phases of clinical research • Clinical trial • Patient • Heart failure • Heart failure • Redox • Ejection fraction • Bone fracture • Blood • Blood pressure • Heart failure • Clinical trial • Patient • Ejection fraction • Bone fracture • Blood • Diastolic heart failure • Bayer • Imipenem/cilastatin • Combination drug • Investigational New Drug • Β-Lactamase inhibitor • Imipenem/cilastatin • Antibiotics • Brand • Imipenem/cilastatin • Therapy • Urinary tract infection • Gram-negative bacteria • Antimicrobial resistance • Therapy • Alternative medicine • Food and Drug Administration • Merck & Co. • New drug application • New drug application • Priority review (FDA) • Prescription Drug User Fee Act • Food and Drug Administration • Merck & Co. • New drug application • Prescription Drug User Fee Act • Merck & Co. • Phases of clinical research • Clinical endpoint • Therapy • Imipenem • Infection • Therapy • Nephrotoxicity • Infection • Food and Drug Administration • Food and Drug Administration Safety and Innovation Act • Fast track (FDA) • Therapy • Hospital-acquired pneumonia • Bacterial pneumonia • Medical ventilator • Bacterial pneumonia • Merck & Co. • Immunity (medical) • Immunotherapy • In vivo • Human body • Immune system • Disease • Z.Vex Effects • Immune system • Natural selection • Antigen • Sensitivity and specificity • Cytotoxicity • White blood cell • Chronic condition • Schering-Plough • Multinational corporation • Revenue • Pet • Cat • Livestock • Revenue • Internet • Divestment • Population growth • Income • Urbanization • Product (business) • Revenue • Economic growth • Industry • Economic development • Software deployment • Innovation • Product (business) • Technology • Productivity • Profit (accounting) • Customer • Business operations • Product (business) • Pharmaceutical industry • Vaccine • Health administration • Digital electronics • New product development • Pharmaceutical industry • Collaboration • Merck & Co. • License • Leadership • Veterinary medicine • Vaccine • Flea • Cat • Dog • Pet • Vaccine • Livestock • Ruminant • Cattle • Sheep • Poultry • Domestic pig • Hypertension • Economic growth • Vaccine • Pharmaceutical drug • Innovation • Pharmaceutical drug • Technology • Effectiveness • Pharmaceutical drug • Merck & Co. • EU three • Animal identification • Veterinary physician • Pet • Management • Health • Quality of life • Livestock • Pet • Globalization • Protein • Industrial engineering • Meat • Food safety • Traceability • Disease • Productivity • Animal husbandry • Health • Fertility • Disease • Intelligence • Sustainability • Natural resource management • Fish • Aquaculture • Pet door • Revenue • Revenue • Pembrolizumab • Pipeline transport • S15 (ZVV) • Platoon • Merck & Co. • Revenue • Interest rate • Revenue • Revenue • Economic growth • Sitagliptin • Revenue • Sitagliptin • Sitagliptin • Sitagliptin/metformin • Merck & Co. • Revenue • Revenue • Company • Knowledge • Agriculture • Merck & Co. • Sitagliptin • Transparency report • Drug • Pembrolizumab • Juggernaut (comics) • Zoster vaccine • Elbasvir/grazoprevir • Company • Property • Economic growth • Pembrolizumab • Profit (accounting) • Globalization • Pharmaceutical drug • Market (economics) • Merck & Co. • Finance • Profit (accounting) • Merck & Co. • Company • Natural resource • Economic growth • Business model • Organizational culture • Agile software development • Economic efficiency • Labour market flexibility • Equal opportunity • Company • Capacity utilization • First-mover advantage • Industry • Innovation • Social change • Merck & Co. • Automation • Innovation • Customer • Supply chain • Back office • Accounting standard • Accounting standard • Operating margin • Return on capital • Fiscal year • Merck & Co. • Globalization • Restructuring • Education • Manufacturing • Globalization • Real estate • Education • Restructuring • Honda S800 • Tax • Profit (accounting) • Profit (accounting) • Free cash flow • Merck & Co. • Investment • Research and development • Mergers and acquisitions • Strategic management • Collaboration • Manufacturing • Capacity utilization • Information technology management • Shareholder • Return on investment • Stock • Dividend payout ratio • Sustainability • Term (time) • Revenue • Economic growth • Operating margin • Economic growth • Value (economics) • Capital (economics) • Economic system • Futures contract • Economic growth • Revenue • Profit (accounting) • Shareholder • Rate of return • Earnings • Valuation (finance) • Accounting standard • Accounting standard • Merck Group • Accounting standard • Accounting standard • Accounting standard • Accounting standard • Standard cost accounting • Mergers and acquisitions • Research and development • Cost • Restructuring • Cost • Profit (accounting) • Futures contract • Accounting standard • BMW M54 • 1,000,000,000 • 1,000,000,000 • Mergers and acquisitions • Accounting standard • S85 (Berlin) • Accounting standard • Expense • Cost of goods sold • SG&A • Expense • Research and development • Expense • Debt restructuring • Cost • Management • Accounting standard • Takeover • Debt restructuring • Takeover • Accounting standard • Platoon • Therapy • Tilos • Therapy • Management • Company • Accounting standard • SG&A • Expense • Accounting standard • Research and development • Expense • Accounting standard • Operating margin • Return on investment • Management • Accounting standard • Mergers and acquisitions • Management • Accounting standard • Net profit • Profit margin • Accounting standard • Expense • Fixed cost • Tax • Debt restructuring • Cost • Accounting standard • Mergers and acquisitions • Accounting standard • Mergers and acquisitions • Cost • Performance management • Futures contract • Mergers and acquisitions • Collaboration • Profit (economics) • Industrial engineering • Revenue • Cost • Accounting standard • Takeover • Cost • Research and development • Business cycle • Mergers and acquisitions • Profit (accounting) • Long run and short run • Profit (accounting) • Accounting standard • Earnings per share • Accounting standard • Accounting standard • Earnings per share • Dividend • Share (finance) • Price–earnings ratio • Shareholder • Rate of return • Stock • Accounting standard • Earnings per share • Accounting standard • Earnings per share • Accounting standard • Earnings per share • Accounting standard • Accounting standard • Stock • Dividend • Stock • Rate of return • Ion • Rate of return • Pembrolizumab • Patent • European Union • Revenue • Economic growth • Management • Pembrolizumab • Oncology • Revenue • Pembrolizumab • Patent • Sitagliptin • Sitagliptin/metformin • Risk • Merck & Co. • Management • Finance • Performance management • Company • Return on investment • Shareholder • Corporation • Stock •