This chart shows why everyone on Wall Street is so worried about the yield curve - 3 minutes read

Wall Street's top rated economist Ed Hyman just called the yield-curve inversion "the number one" market risk, and this chart shows why.

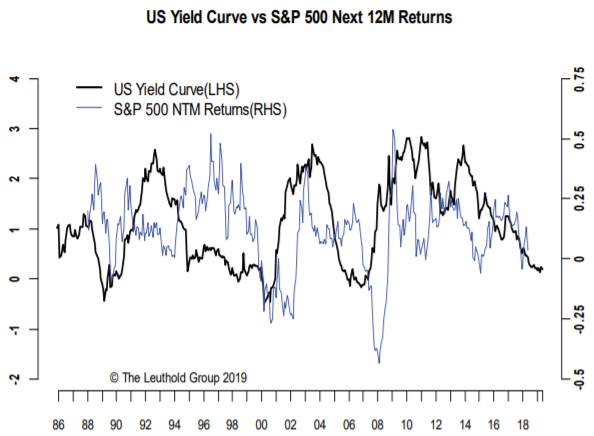

Going back to 1986, when the yield curve turned flatter drastically and eventually inverted, the S&P 500 tends to go into a downward spiral within the next 12 months, according to The Leuthold Group.

Take 2004 when the yield spread started falling from its highs. The flattening didn't get the market's attention until about 2006 when the curve inverted, and the recession hit exactly a year later.

There's "a positive relationship between the yield curve and the S&P 500's next 12-month returns," said Chun Wang, Leuthold's senior analyst and portfolio manager, in a note. "Recession or not, a flatter curve generally bodes ill for future stock market performance. The current trend in the yield curve is likely to cap the upside for stocks in the next 12 months."

Keep in mind that Wang tested the spread between the 10-year and 2-year Treasury yields, not the 3-month and 10-year yield curve that's currently inverted. Yield-curve inversion has been a reliable recession signal closely watched by experts and the Federal Reserve.

.1560527243900.jpeg)

The shape of the curve is exuding a bad omen for the stock market if history is any guide. The yield on the 10-year Treasury hit a 20-month low last week as the escalated trade battles triggered a broad flight to safety. The low benchmark rate has flattened the 2-year/10-year yield curve to only about 23 basis points on Friday. In December, the spread hit the lowest level since the financial crisis during a massive sell-off. Yet despite the flattening, the S&P 500 is still up 15% this year.

Troublesome banks

The other overlooked element of the yield curve is that it's now the dominant driver for an important group of stocks: banks, the analyst pointed out.

Bank stocks have significantly lagged the overall market regardless of interest rates' ebbs and flows since the start of 2018 and they moved almost in tandem with the flattening yield curve, Wang said.

"The market is much more worried about the curve than the rate level...bank stocks are basically a proxy for whatever equity investors are most worried about in the bond market," Wang said. If the spread between 10-year and 2-year yield dips into negative territory, "the implication for bank stocks is quite troubling," he added.

Bank stocks have underperformed recently as the chance of rate cuts soared amid fears of an economic slowdown and ongoing trade war. Lower interest rates could wreck large-cap bank earnings by as much as 10%. The SPDR S&P Bank ETF has fallen 2.8% in the past month and 4.8% in the last three months, while the S&P 500 gained 1.7% and 2.6% in those periods.

"An escalation of trade war without offsetting rate cuts, a much stronger dollar, and flatter foreign-yield curves could all provide the final push into full inversion. We recommend watching bank stocks closely, given the special role they take right now," Wang said.