The Chemist's Quality Closed-End Fund Report - June 2019 - 6 minutes read

The Chemist's Quality Closed-End Fund Report - June 2019

The Chemist's Quality Closed-End Fund Report - June 2019This article was first released to CEF/ETF Income Laboratory subscribers 1 month ago, so data may be out of date. Please check latest data before making investment decisions.

Quantitative screens help to rapidly narrow down attractive candidates from the database of 500-plus closed-end funds [CEFs] for further due diligence and investigation.

Based on feedback from members, it seems that a very many number of investors, understandably, place a great emphasis on coverage and return of capital. While I'm not going to rehash the entire ROC argument here (it is suffice to say that the issue is much more complicated than "ROC = bad"), some investors may consider a fund with over 100% coverage to be attractive simply because they know that the distributions are being covered by earnings. Such a fund may be at lower risk of a distribution cut, which can cause devastating impacts to a fund's market price, and may even afford to raise its distribution in the future.

What does the "quality" indicate? Simply put, it means that the distribution coverage is greater than 100%. However, please note these caveats: Firstly, coverage ratios are calculated using earnings data from CEFConnect. While there are sometimes discrepancies with CEFConnect's data, this allows us to automate the calculation process for the entire universe and we consider it to be sufficiently reliable for a preliminary screen anyway. Before buying or selling any fund, it is recommended to independently verify the coverage ratios from the individual fund annual/semi-annual reports themselves.

Secondly, having a coverage ratio >100% does not guarantee that the fund's distribution is secure. Many funds reduce their distributions periodically in line with market conditions in order to maintain good coverage. Thirdly, a coverage cut-off ratio of 100% is, ultimately, an arbitrary number. A fund with 99.9% coverage will be excluded from the rankings, whereas funds with 100.1% coverage will be considered, even though only a sliver of coverage separates the two.

The coverage ratio is calculated by dividing the earnings/share number provided by CEFConnect on the "distributions" tab by the distribution/share. CEFdata also provides earning coverage numbers as well.

I hope that these rankings of quality CEFs will provide fertile ground for further exploration.

Data were taken from the close of June 14, 2019.

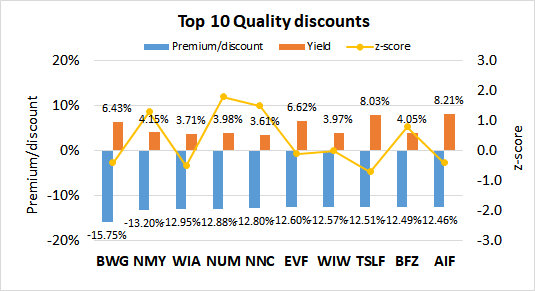

The following data show the 10 CEFs with the widest discounts and coverage >100%. Yields, z-scores and leverage are shown for comparison.

CEFs with the lowest z-scores are potential buy candidates. The following data show the 10 CEFs with the lowest z-scores. Premium/discount, yields and leverage are shown for comparison. Only funds with coverage >100% are considered.

Some readers are mostly interested in obtaining income from their CEFs, so the following data presents the top 20 highest yielding CEFs. I've also included the premium/discount and z-score data for reference. Before going out and buying all 10 funds from the list, some words of caution: [i] higher yields generally indicate higher risk, and [ii] some of these funds trade at a premium, meaning you will be buying them at a price higher than the intrinsic value of the assets (which is why I've included the premium/discount and z-score data for consideration). Only funds with coverage >100% are considered. To make the charts more manageable I've split the funds into two groups of 10.

For possible buy candidates, it is probably a good idea to consider both yield and discount. Buying a CEF with both a high yield and discount not only gives you the opportunity to capitalize from discount contraction, but you also get "free" alpha every time the distribution is paid out. This is because paying out a distribution is effectively the same as liquidating the fund at NAV and returning the capital to the unitholders. I considered several ways to rank CEFs by a composite metric of both yield and discount.

The simplest would be yield + discount, however I disregarded this because yields and discounts may have different ranges of absolute values and a sum would be biased towards the larger set of values. I finally settled on the multiplicative product, yield x discount. This is because I consider a CEF with 7% yield and 7% discount to be more desirable than a fund with 2% yield and 12% discount, or 12% yield and 2% discount, even though each pair of quantities sum up to 14%. Multiplying yield and discount together biases towards funds with both high yield and discount. Since discount is negative and yield is positive, the more negative the "D x Y" metric, the better. Only funds with >100% coverage are considered.

This is my favorite metric because it takes into account all three factors that I always consider when buying or selling CEFs: yield, discount and z-score. The composite metric simply multiplies the three quantities together. A screen is applied to only include CEFs with a negative 1-year z-score. As both discount and z-score are negative while yield is positive, the more positive the "D x Y x Z" metric, the better. Only funds with >100% coverage are considered.

Disclosure: I am/we are long THE PORTFOLIOS. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Source: Seekingalpha.com

Powered by NewsAPI.org

Keywords:

Chemistry • Closed-end fund • Exchange-traded fund • Database • Due diligence • Feedback • Investor • Return of capital • Ratio • Data • Data • Scientific method • Universe • Insurance • Insurance • Ratio • Distribution (business) • Market economy • Goods • Insurance • Insurance • Insurance • Insurance • Sliver (film) • Insurance • Ratio • Income • Stock • Invoice • Standard score • Leverage (finance) • Standard score • Trade • Data • Standard score • Insurance • Leverage (finance) • Insurance • Income • Data • Insurance • Standard score • Data • Financial risk • Trade • Insurance • Price • Intrinsic value (finance) • Asset • Insurance • Standard score • Data • Funding • Insurance • Funding • Trade • Idea • Discounts and allowances • High-yield debt • Discounts and allowances • Opportunity cost • Discounts and allowances • Recession • Alpha (finance) • Liquidation • Net asset value • Capital (economics) • Metric (mathematics) • Yield (finance) • Discounts and allowances • Yield (finance) • Discounts and allowances • Yield (finance) • Range (mathematics) • Absolute value • Addition • Set (mathematics) • Multiplication • Multiplication • Multiplication • Standard score • Standard score • Standard score • Seeking Alpha • Stock •